Fraud protection.

Now it's personal.

ANZ Falcon® technology monitors millions of transactions every day to help keep you safe from fraud.

Falcon® is a registered trademark of Fair Issac Corporation.

Fraud protection.

Now it's personal.

ANZ Falcon® technology monitors millions of transactions every day to help keep you safe from fraud.

Falcon® is a registered trademark of Fair Issac Corporation.

Fraud protection.

Now it’s personal.

ANZ Falcon® technology monitors millions of transactions every day to help keep you safe from fraud.

Falcon® is a registered trademark of Fair Isaac Corporation.

With credit cards come big responsibilities, which is why it’s important to understand how they work. Credit card education is an online series that explores credit card interest, making payments, balance transfers and more.

![]()

Featured

Wondering if a credit card is the right choice for you? Find out how they work, their perks and pitfalls and how to use them wisely.

Article

In this article, we explain how to apply for an ANZ credit card and the information you’ll need to complete your application.

Article

Choosing a credit card should never be done on a whim. Make sure you compare fees and charges, interest rates and benefits so that your decision is an informed one.

Article

Applying for a new credit card? Make sure you consider a credit limit that aligns with your spending habits and your ability to repay your card balance.

Article

Familiarising yourself with your credit card statement is crucial. It can help you keep track of your spending, make your repayments on time, avoid fees and interest charges, and more.

![]()

Featured

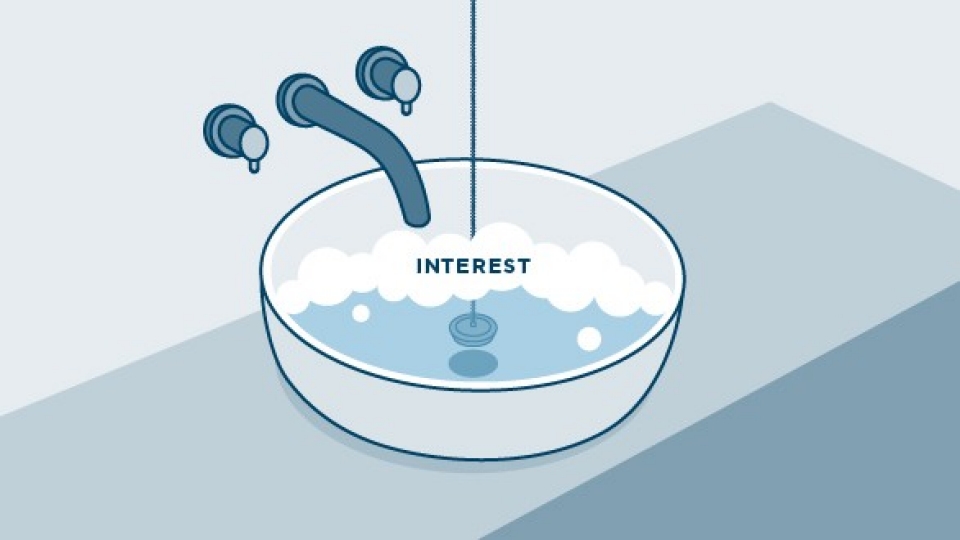

Understanding credit card interest is a bit like running a bath. It’s important to keep your eye on it. Let’s dip into some helpful tips.

Article

Making the most of your interest-free period can help you save money and manage your finances better. We explain what it is, how to maximise it and some common pitfalls to avoid.

Article

Paying credit card interest bites big time, especially when it can be avoided. In this article, we look at how to minimise your credit card interest – and how to avoid paying it altogether.

![]()

Featured

Setting up Due Date reminders or a direct debit arrangement could be helpful if you want to develop a regular rhythm of paying off a credit card. Get a little taste of how credit card payments work.

Article

Familiarising yourself with industry terms and practices can help you minimise or avoid paying interest on your credit card purchases. In this article, we help demystify the lingo and more.

Article

As a credit cardholder, you’re only obligated to pay the Minimum Monthly Payment each month. However, if you take this approach, it’ll take you longer to pay off your card and you’ll end up paying more interest.

Article

Learn about credit card cash advances: what they are, the costs involved, how they work, what counts as a cash advance, and why you may want to avoid them altogether.

Article

A little knowledge can go a long way towards helping you take control of your budget and your credit card. These hacks could help you gain a new understanding of your spending habits.

Featured

Just like fitness and food, there are good habits and bad habits when it comes to spending. To avoid credit card debt, it may help to evaluate where you stand.

Article

Card debt looming over your head? Or perhaps you want to get off on the right foot with your first credit card, armed with strategies to help you pay off the balance in full each month.

![]()

Featured

Brush up on balance transfers before you make a decision about a promotional balance transfer offer. Dig into these helpful tips.

Article

A promotional Balance Transfer offer, if used wisely, may make it easier for you to consolidate your credit card debt and pay it off sooner.

![]()

Featured

A useful guide on credit card fraud. Discover what it is and what to do if you fall victim. We also look at how we protect you.

Article

There are specific guidelines about when you can use your personal ANZ credit card for gambling transactions.

Article

A credit card can affect your credit score both positively and negatively over time, so it’s important to learn how to use them responsibly.

We may provide you with links to general articles and tools that may help you but any advice does not take into account your objectives, personal needs and financial circumstances and does not constitute financial advice or a recommendation. Before considering if any product is right for you, you should take into account your personal needs and financial circumstances and consider whether it is appropriate for you.